Appoint auditor

Document overview

England & Wales

England & Wales Scotland

Scotland

- Length:5 pages (770 words)

- Available in:

Microsoft Word DOCX

Microsoft Word DOCX Apple Pages

Apple Pages RTF

RTF

If the document isn’t right for your circumstances for any reason, just tell us and we’ll refund you in full immediately.

We avoid legal terminology unless necessary. Plain English makes our documents easy to understand, easy to edit and more likely to be accepted.

You don’t need legal knowledge to use our documents. We explain what to edit and how in the guidance notes included at the end of the document.

Email us with questions about editing your document. Use our Lawyer Assist service if you’d like our legal team to check your document will do as you intend.

Our documents comply with the latest relevant law. Our lawyers regularly review how new law affects each document in our library.

About this set of documents

Most private limited companies are not required to have an auditor. That is because they qualify as “small companies” under the CA 2006 and are not charities or members of a group of companies.

The definition of a small company is one that is not ineligible to be one in the current accounting year, nor was ineligible in the previous, and it meets two of three criteria:

Turnover less than £10.2m (before January 2016: less than £6.5m)

Total assets less than £5.1m (before January 2016: less than £3.26m)

Number of employees fewer than 50

A company can choose to be audited. The reason for this choice is often to give one or more shareholders or stakeholders confidence in the accounting of the organisation. For example, a large shareholder who is not a director may ask for an audit to add a level of information that can help satisfy him or her that the board is looking after his or her investment. Or the company may have social goals and may want to appear transparent in all dealings. In these cases, an appointment may give confidence even though the auditor will have no contractual liability.

The audit process does not involve preparation of the accounts or the filing of them at Companies House, although the accounting firm that carries out the audit may also prepare the final accounts.

The advantage of a formal appointment is simply that information obtained by search at Companies House shows that you have done so.

The Companies Act 2006 allows you to appoint an auditor in three ways: by directors’ resolution, in members’ general meeting or by way of written resolution. We have taken advantage of the flexibility in the law and provide you with 3 sets of documents within one. These are straightforward, cover the whole procedure, are effective, and are in plain English of course.

Procedures that can be followed using these documents

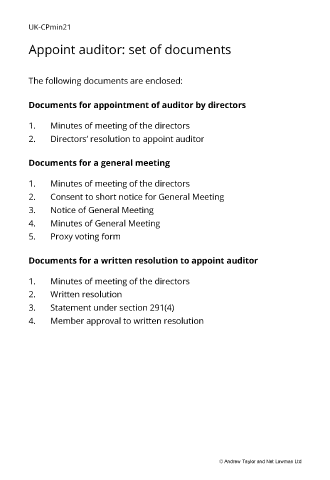

In this pack we have provided the documents required for each of the three procedures. Follow any one by using the set of documents for it.

Appointment by directors

- Minutes of the meeting of the board of directors

- Directors’ resolution to appoint the auditor

By passing a motion in a general meeting of members

- Minutes of the meeting of the directors

- Consent to short notice for the General Meeting

- Notice of the General Meeting

- Minutes of the General Meeting

- Proxy voting form

Written resolution

- Minutes of the meeting of the directors

- Written resolution

- Statement under section 291(4)

- Member approval to the written resolution

Key features

- suitable for any of the three procedures

- provides an option for calling a members meeting with a short notice period

- contains modern provisions in plain English

- allows you to construct your minutes and resolutions to suit your exact business needs

- full of practical and commercial help and suggestions

- save you time and worry as you make your way through each document in turn

Service contract

After the appointment of the auditor, you will additionally need to have a service contract with the firm. This is required to regulate finer points in detail. Most accountancy firms use a standard contract, the contents of which are suggested by a regulatory association, and which is often presented as an engagement letter.

Talk to us about this document

Talk to us about this document

We are happy to answer any questions you have. Arrange for us to call you.

Choose the level of support you need

Document Only

This document

This document - Detailed guidance notes explaining how to edit each paragraph

Lawyer Assist

- This document

- Detailed guidance notes explaining how to edit each paragraph

- Unlimited email support - ask our legal team any question related to completing the document

- Review of your edited document by our legal team including:

- reporting on whether your changes comply with the law

- answering your questions about how to word a new clause or achieve an outcome

- checking that your use of defined terms is correct and consistent

- correcting spelling mistakes

- reformatting the document ready to sign

Bespoke

- A document drawn just for you to your exact requirements

- Personalised service provided by an experienced solicitor

- Free discussion before we provide an estimate, for you to ask questions and for us to understand your requirements

- Transparent fees - a fixed fee for the basic work, a fixed hourly rate for new or changed instructions, and no charge for office overheads or third party disbursements

- Careful and thorough consideration of your circumstances and your consequent likely practical and legal requirements

- Provision of options that you may not have considered with availability for discussion

- Help and advice woven into the fabric of our service so that you can make the best decisions

All rights reserved